In the bustling landscape of American consumerism, credit cards have long been the ubiquitous tool for financial transactions. They offer convenience, flexibility, and seemingly endless purchasing power. However, beneath the veneer of prosperity lies a growing crisis that threatens to unravel the economic fabric of the nation. The signs are clear: the credit card bubble in America is on the verge of popping.

Table of contents

Skyrocketing Credit Card Defaults

A Grim Reality Unveiled

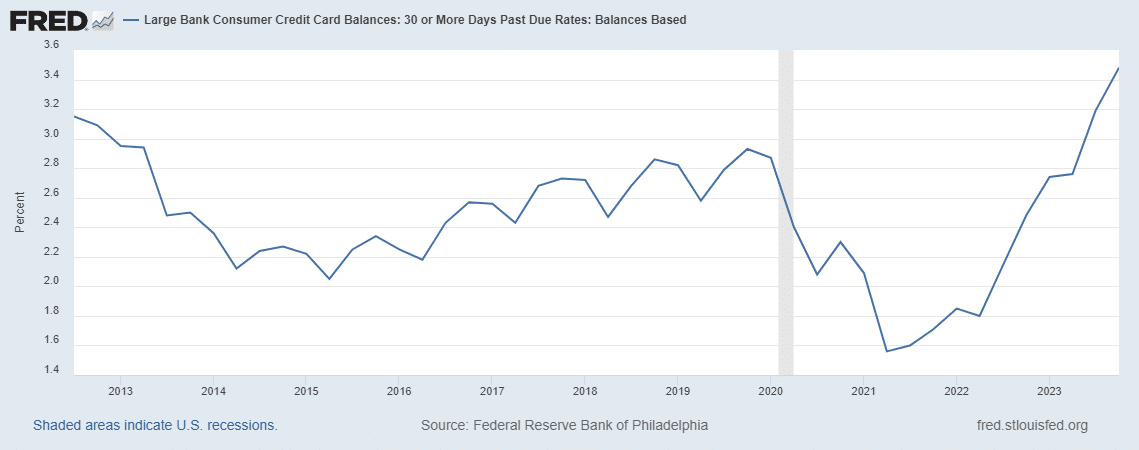

Recent data from the Federal Reserve paints a grim picture of the state of American finances. Credit card default rates are skyrocketing, indicating a troubling trend of consumers failing to meet their financial obligations. According to a study conducted by the Philadelphia Fed, nearly 3.5% of card balances were at least 30 days past due, marking the worst delinquency rates on record. Moreover, the percentage of individuals making only the minimum payment on their credit cards has spiked to a series high, signaling widespread consumer stress.

Echoes of Past Crises

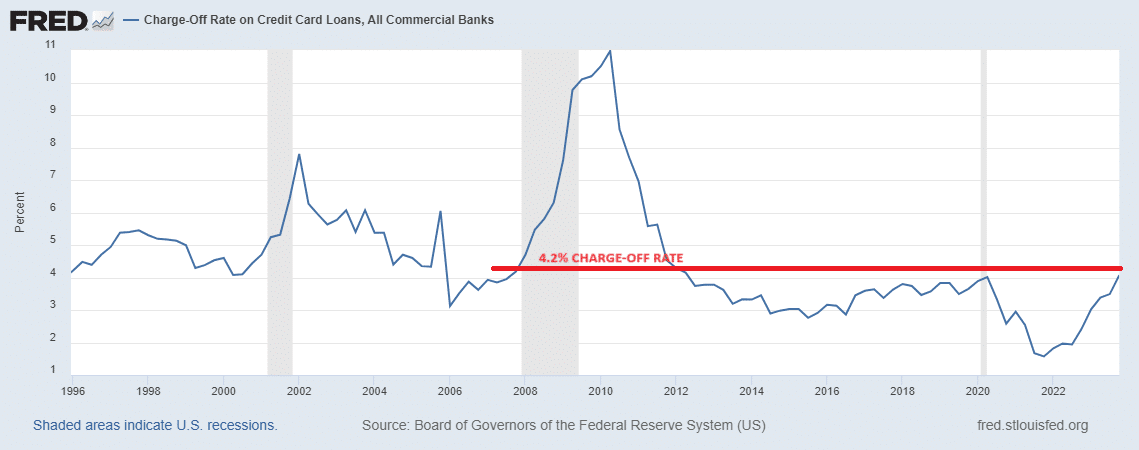

The parallels between the current situation and the financial crisis of 2007-2008 are unsettlingly familiar. During that tumultuous period, the charge-off rate on credit card loans hit 4.2%, that marked the start of the Great Recession. We are seeing the charge-off rate approaching this level once again. History serves as a cautionary tale, reminding us that ignoring such warning signs can have catastrophic consequences for the economy.

The Burden of Debt

Ballooning Credit Card Balances

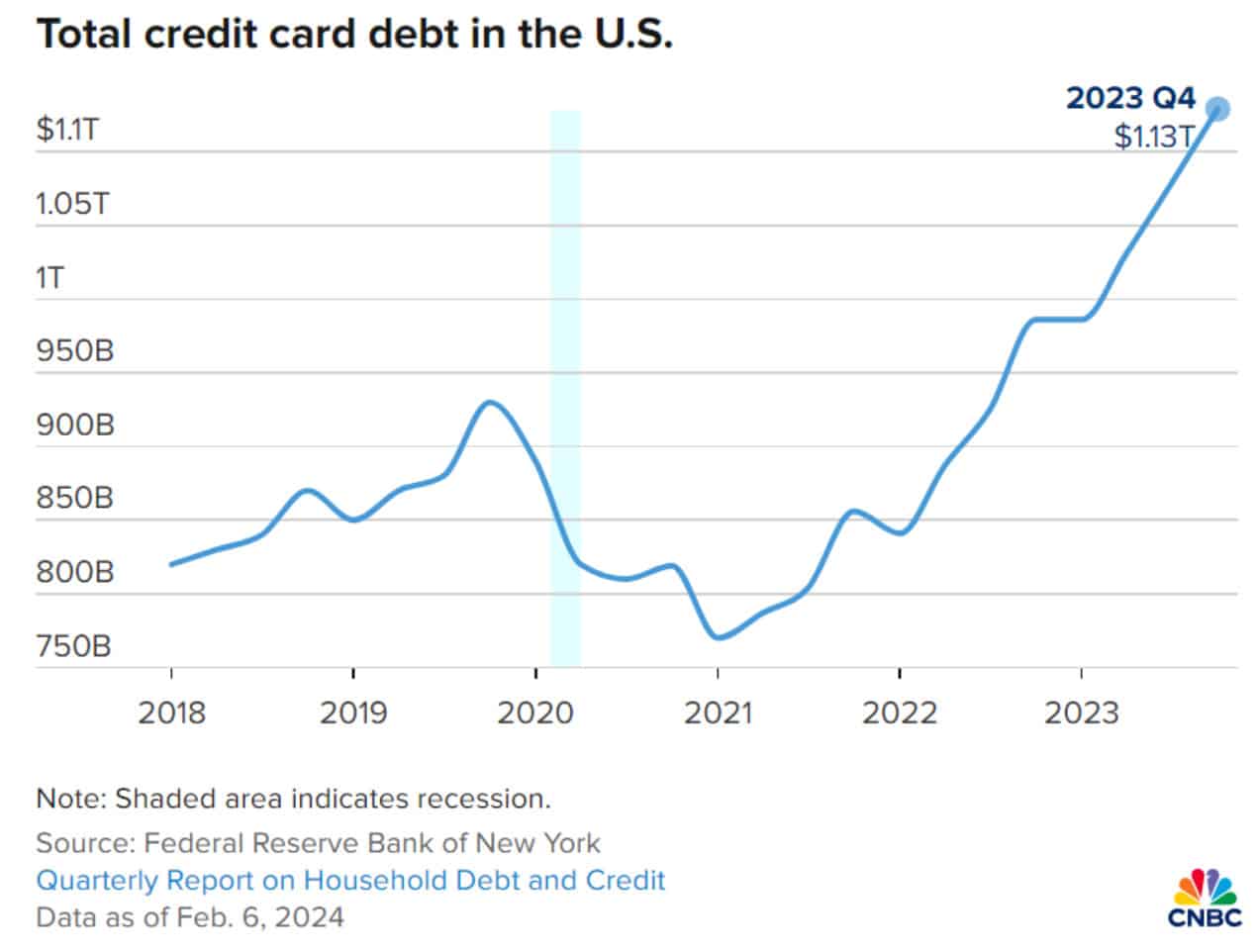

The burden of credit card debt weighs heavily on the shoulders of American households. CNBC reports that credit card debt soared to a staggering $1.13 trillion earlier this year, reaching an all-time high. This represents a 20% increase from pre-pandemic levels, highlighting the growing reliance on credit to sustain everyday expenses.

Struggling to Keep Up

The surge in credit card balances is compounded by stagnant wages and rising inflation, creating a perfect storm of financial instability. As the cost of living outpaces income growth, many Americans find themselves trapped in a cycle of debt, struggling to make ends meet. The allure of easy credit masks the harsh reality of a shrinking purchasing power.

Rising Interest Rates

A Double-Edged Sword

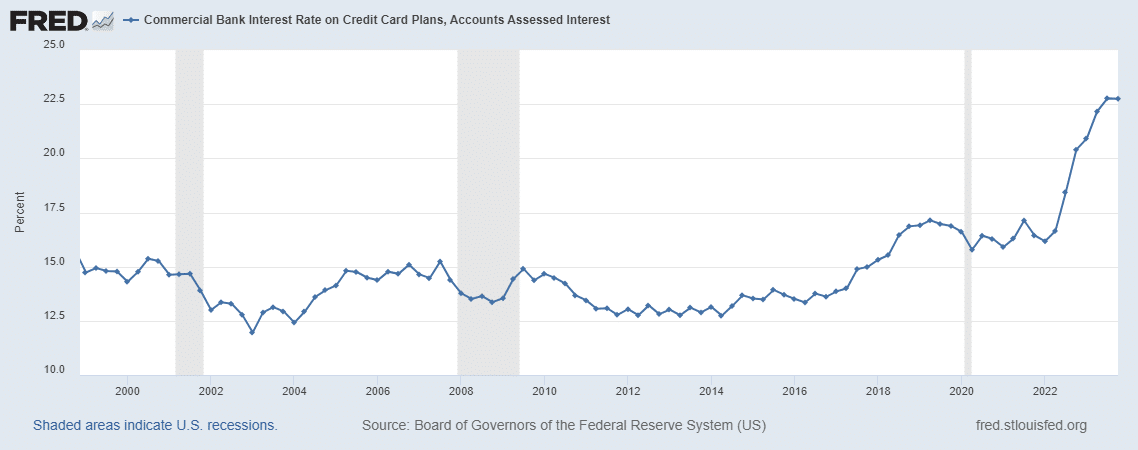

Adding fuel to the fire, interest rates on credit card debt have surged to alarming levels. Commercial bank interest rates on credit card plans averaged a staggering 22% at the beginning of 2024, marking the highest rate in three decades. This sharp increase in borrowing costs further exacerbates the financial strain faced by consumers, making it increasingly difficult to escape the cycle of debt.

The Ticking Time Bomb

The convergence of surging default rates, ballooning credit card balances, and skyrocketing interest rates creates a precarious situation reminiscent of a ticking time bomb. The fragility of the American economy is laid bare, exposing the inherent vulnerabilities lurking beneath the surface. Unless decisive action is taken to address the root causes of this crisis, the consequences could be dire.

The credit card bubble in America is reaching a breaking point, with ominous signs of impending collapse. Skyrocketing default rates, ballooning credit card balances, and soaring interest rates paint a troubling portrait of an economy teetering on the brink. The lessons of the past serve as a stark reminder of the dangers of complacency. It is imperative that we confront these challenges head-on, lest we risk repeating the mistakes of history. The time to act is now, before it’s too late.

💥 GET OUR LATEST CONTENT IN YOUR RSS FEED READER

We are entirely supported by readers like you. Thank you.🧡

This content is provided for informational purposes only and does not constitute financial, investment, tax or legal advice or a recommendation to buy any security or other financial asset. The content is general in nature and does not reflect any individual’s unique personal circumstances. The above content might not be suitable for your particular circumstances. Before making any financial decisions, you should strongly consider seeking advice from your own financial or investment advisor.